Weekly Market Insights

March 27, 2026 Volume 13 Issue 12

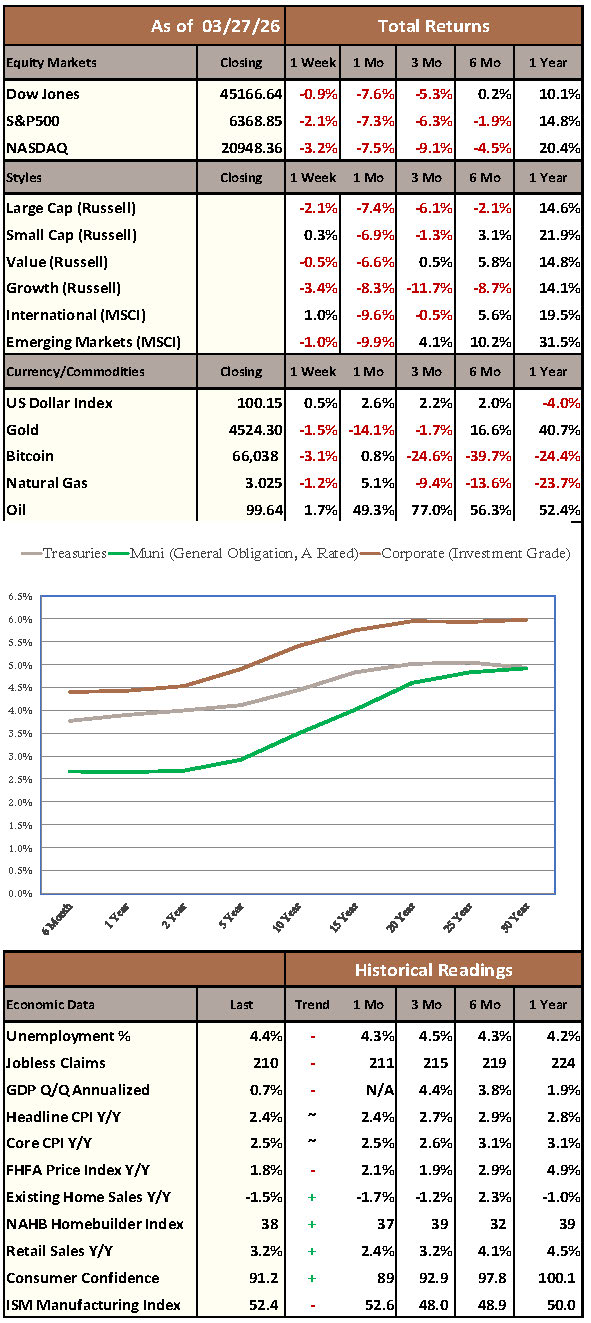

Markets steadied as investors navigated war driven volatility, with risk appetite remaining selective. Small caps outperformed following recent weakness, while large caps were mixed. Energy led on ongoing supply concerns, while Technology and Communications lagged amid rate sensitivity. Utilities and Consumer Staples held up better as defensives. International equities showed relative strength versus the U.S. In fixed income, shorter maturities were steadier than the long end as yields stayed elevated and credit conditions remained stable. Commodities were mixed, with firm crude offset by weaker precious metals. Alternatives diverged, as midstream assets strengthened and listed private equity softened.

The economic backdrop was shaped by energy disruption tied to the Middle East conflict. Transit through the Strait of Hormuz became more controlled, raising insurance costs and complicating fuel flows. These frictions pushed gasoline and diesel prices higher, reinforcing inflation pressures. Labor signals remained mixed, sustaining uncertainty around growth momentum. Corporate earnings showed wide dispersion, particularly among small caps and commodity exposed businesses. Inflation remained central, reinforced by firm PCE measures and pass-through from energy and logistics costs.

Policy dynamics centered on the Federal Reserve as officials weighed tradeoffs created by higher energy prices. Some policymakers allowed for easing if labor conditions weaken, while others emphasized upside inflation risks. Market pricing shifted toward fewer rate cuts and higher odds of hikes. Regulators eased bank capital requirements to support funding markets, while policymakers relied on an exchange-based reserve release to manage energy pressures. Separately, the Senate advanced measures intended to end the government shutdown and sent the legislation back to the House, leaving near term fiscal outcomes dependent on next steps.

Across markets, investors continued to weigh transit disruption, policy uncertainty, and inflation risks as conditions remained fluid.

Have a great weekend!

The data and commentary provided herein is for informational purposes only. No warranty is made with respect to any information provided. It is offered with the understanding that Hilltop Holdings Inc., PlainsCapital Corporation, Hilltop Securities and PlainsCapital Bank (collectively “PCB”) are not, hereby, rendering financial and/or investment advice, and use of the same does not create any relationship with PCB. This is neither an offer to sell nor a solicitation of an offer to buy any securities that may be described or referred to herein. PCB does not provide tax or legal advice. Please consult your own tax or legal advisor regarding your specific situation. Whether any of the information contained herein applies to a specific situation depends on the facts of that particular situation. Investment and estate planning and management decisions may have significant financial consequences and should be made only after consulting with professionals qualified to offer legal, accounting and taxation advice. Neither this document nor any portion of its content’s supplements, amends or modifies any account agreement with PCB. Unless otherwise noted:

*All economic release data referenced from public sources believed to be accurate. *The source of data for all charts/graphs included in this presentation is Bloomberg LP. *Figures quoted represent monthly changes (m/m) and are seasonally adjusted.