Recent U.S. actions in Venezuela and Iran suggest efforts to reinforce the dollar’s role in global energy markets. Supporters point to Venezuela’s hydrocarbon reforms after Maduro’s capture, the U.S.-Iran conflict disrupting energy flows, and declining gold prices since January. Expanded access to Venezuelan oil could boost dollar-based markets, while falling gold prices indicate reduced demand for alternatives to the dollar.

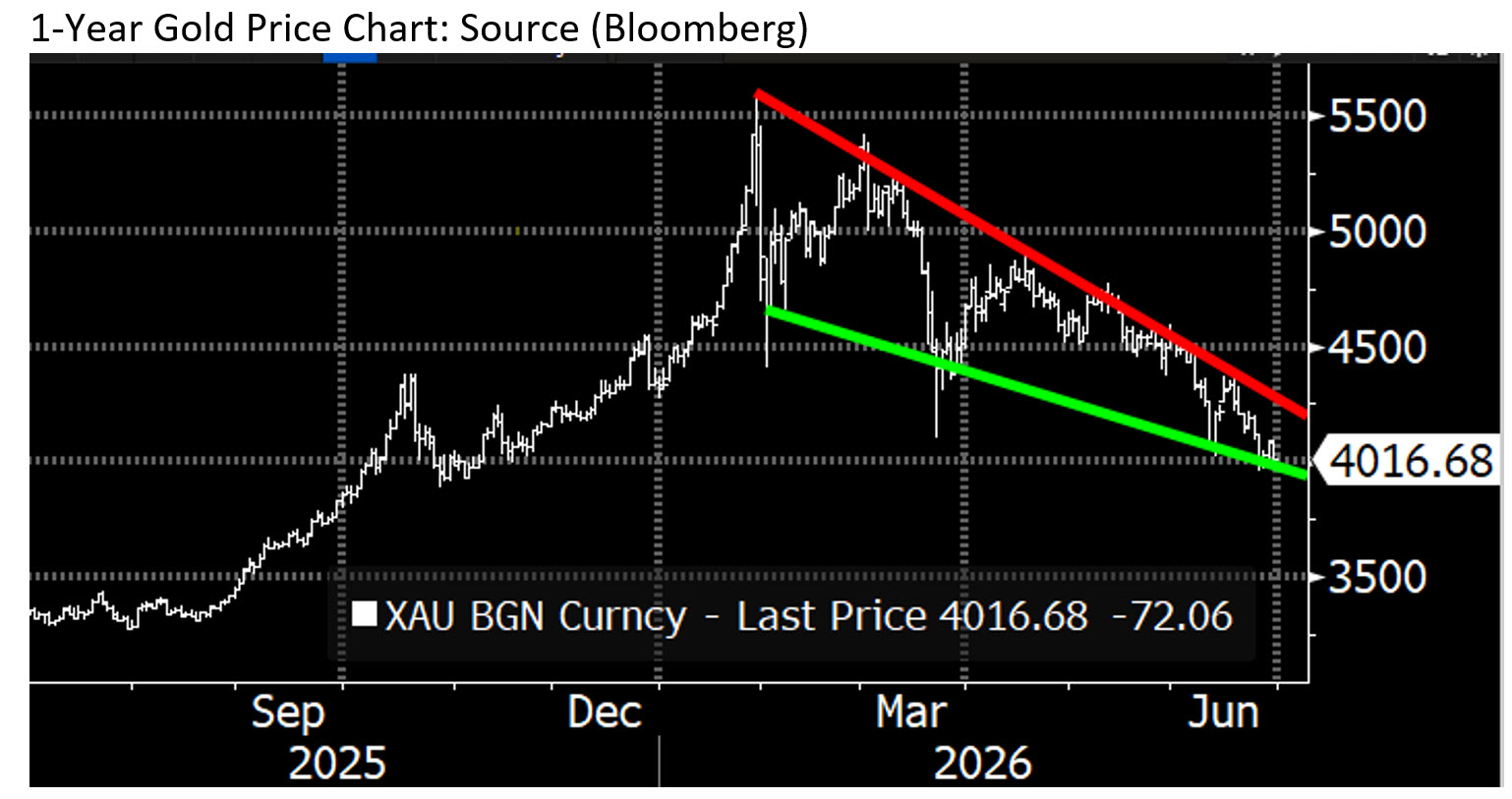

Gold hit a record $5,595.47/oz on January 29, 2026, closing at $4,008.02/oz on June 30—about 28% below its peak. Despite this decline, geopolitical risks remained high with ongoing U.S.-Iran conflict, Venezuelan unrest, and emerging-market stress, which usually boost safe-haven demand. This anomaly underpins the dollar-hegemony thesis, but evidence remains limited. These events are better explained by strategic, monetary, and energy market forces than by a coordinated effort to reshape the global monetary order.

Venezuela’s National Assembly passed sweeping hydrocarbons reforms on January 29, 2026 — the same day gold reached its all-time high of $5,595.47/oz — with the law signed by acting President Delcy Rodríguez the following day. The reforms open the country’s oil sector to greater foreign investment, expand private-sector participation, and grant greater autonomy in production and sales, marking the most significant overhaul of Venezuela’s hydrocarbons framework in more than two decades. Critically, this reform did not stem from an independent Venezuelan policy pivot: it followed the U.S. military operation that led to Maduro’s capture and was implemented under a government explicitly aligned with U.S. economic plans.

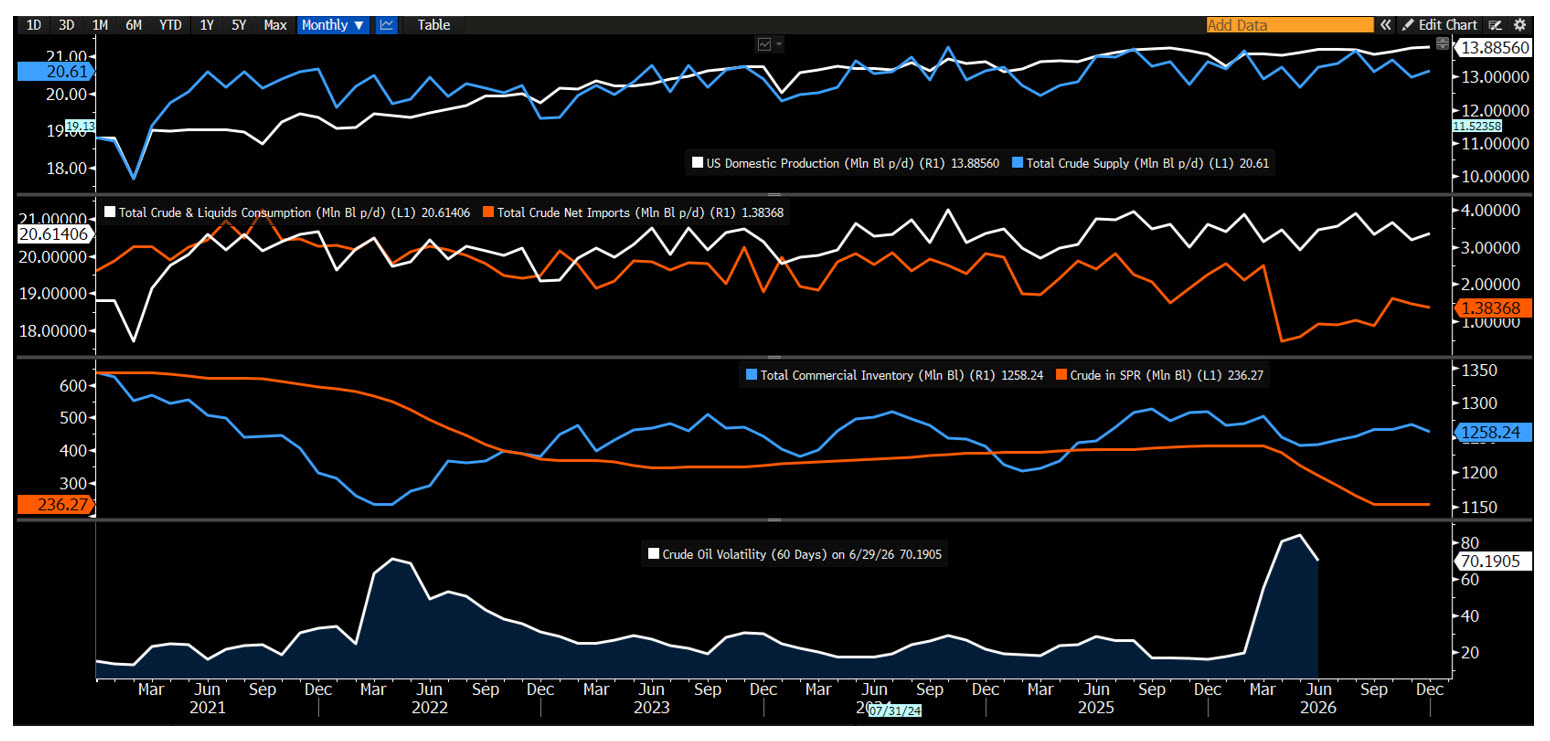

Despite the significance of the legal reform, Venezuela’s energy sector faces substantial operational and financial challenges. Restoring production capacity to historical peak levels is estimated to require more than $100 billion in investment over many years. Major international operators have remained cautious: Exxon described Venezuela as “uninvestable” as recently as January, and Chevron’s CEO stated in March that “more groundwork” is needed before large-scale investment commitments are viable. Although Venezuelan crude exports reached a seven-year high of 1.17 million barrels per day in June, much of this increase was supported by the release of floating storage accumulated before Maduro’s capture, rather than by sustained gains in productive capacity. Furthermore, international traders, including Trafigura and Vitol, are actively marketing Venezuelan crude to Asian buyers — limiting the argument that these developments primarily strengthen Western, dollar-denominated energy markets.

The Iran dimension of the thesis is similarly difficult to sustain on the evidence. The U.S. conducted active military operations against Iran beginning in late February 2026, including strikes on Kharg Island and a naval blockade of the Strait of Hormuz that materially disrupted global oil flows. An interim peace agreement was signed on June 14, followed by a 60-day sanctions waiver issued on June 22 that explicitly permits Iran to sell crude and petroleum products, with payments accepted in multiple currencies. Iran has indicated its intention to maximize exports under the current framework and to sell oil to all countries except Israel.

The outcome has been a significant increase in global oil supply rather than its restriction: commercial shipping through the Strait of Hormuz has surged to more than 10 million barrels per day with U.S. military support, catching Tehran off guard and underscoring its now-limited ability to halt traffic through the corridor. Taken together, these developments appear more consistent with efforts to stabilize global energy supplies than with a strategy focused on consolidating dollar-denominated oil markets. Notably, during the conflict, portions of Hormuz transit fees were settled in yuan-denominated arrangements — a concrete example of dollar alternatives gaining traction precisely during the period the thesis claims dollar dominance was being reinforced.

Developments in monetary policy offer a compelling explanation. The Federal Reserve, under Chair Kevin Warsh, has adopted a hawkish stance in H1 2026, with markets expecting further rate hikes. The 10-year U.S. real yield was 1.93% on July 1, providing a positive return and acting as a headwind for non-yielding assets like gold. The DXY strengthened in three of five months from February to June, with March and June seeing the largest gains (+2.4% and +2.3%), coinciding with significant declines in gold. Rising real yields and dollar appreciation are well-known headwinds for gold, making geopolitical factors unnecessary to explain its performance.

If U.S. actions in Venezuela and Iran had meaningfully reinforced dollar dominance, one would expect to see structural de-dollarization trends stall or reverse. The available evidence points in the opposite direction. A June 30 survey by the Official Monetary and Financial Institutions Forum found that emerging-market reserve managers plan to increase yuan allocations over the next 12–24 months and over the next decade. Utilization of People’s Bank of China yuan swap lines reached a two-year high in Q1 2026. And, as noted above, yuan-denominated settlement arrangements emerged during the Hormuz transit during the Iran conflict. This development is directly at odds with the thesis that the conflict reinforced dollar-based energy markets. The U.S. dollar remains the dominant global reserve and transaction currency, but these trends indicate that structural diversification efforts have not materially reversed.

The theory linking U.S. actions in Venezuela and Iran to a deliberate effort to reinforce dollar dominance identifies a noteworthy sequence of events. Still, it does not establish a clear causal mechanism. A hawkish Federal Reserve, rising real yields, and a strengthening dollar provide a more conventional, evidence-based framework for understanding gold’s performance in H1 2026. Capital requirements constrain the near-term impact on supply from Venezuelan oil, and the oil is flowing to non-Western buyers. The Iran peace deal has expanded global oil supply rather than restricting competing producers. De-dollarization trends have continued uninterrupted.

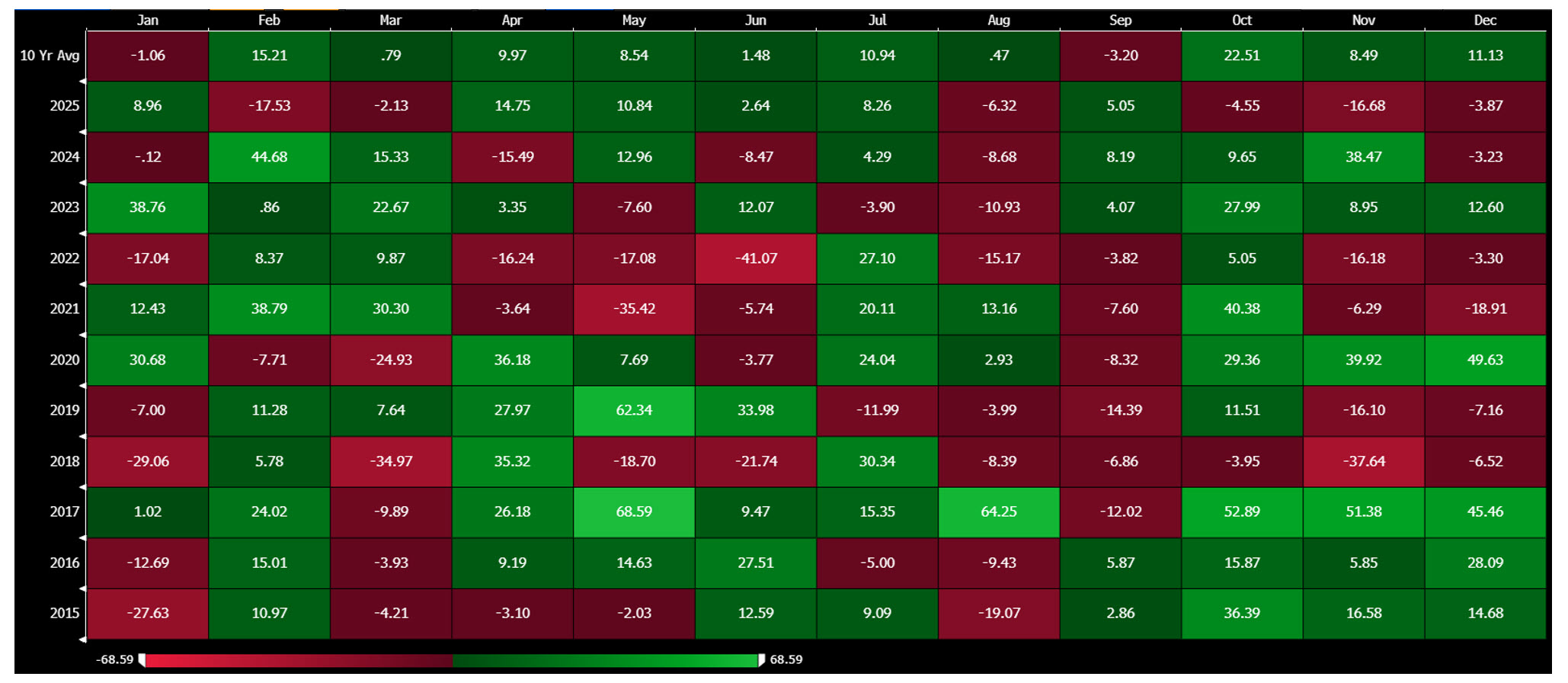

COMMODITY HIGHLIGHTS